Nostalgia has long been a popular tool of marketers. U.K. telecom provider O2 is the latest brand to lean into this trend, partnering with early aughts pop band Steps to stage a surprise flash mob. O2’s campaign is for the Samsung Galaxy Z Flip3 foldable phone, which has the retro look of a flip phone…

Top 3 Streaming Pet Peeves – And Why They Really Happen

Something is rotten in the state of CTV. If you’re a fan of streaming, you probably have a few pet peeves that take you out of the zone, like repeat ads or interruptive ad breaks. Nothing ruins a good show more than thinking it’s trying to sell you something. These problems were solved with a… Continue reading »

The post Top 3 Streaming Pet Peeves – And Why They Really Happen appeared first on AdExchanger.

Why A Single Video Currency Is No Longer Enough

“On TV & Video” is a column exploring opportunities and challenges in advanced TV and video. Today’s column is by Kevin Krim, CEO of EDO. After this exclusive first look for subscribers, the piece will be published in full on AdExchanger.com tomorrow. In 1941, the first true television commercial aired in America, featuring the Bulova… Continue reading »

The post Why A Single Video Currency Is No Longer Enough appeared first on AdExchanger.

2022 M&A Stays Crazy; Apple’s App Privacy Report Lifts The Hood On Trackers

Here’s today’s AdExchanger.com news round-up… Want it by email? Sign up here. The “Solid” In Consolidation Are you sick of hearing about M&A already? TOO BAD! We’ve still got multiple deals being announced on the regular. On Wednesday, the publisher services company OpenWeb – known for operating comment sections and targeting ads by user account IDs… Continue reading »

The post 2022 M&A Stays Crazy; Apple’s App Privacy Report Lifts The Hood On Trackers appeared first on AdExchanger.

M&M’s Updates Mascots to Represent a More ‘Dynamic and Progressive World’

The times are changing, and so are M&M’s well-known mascots. In an effort to better align with today’s emphasis on inclusivity and belonging, the 80-year-old brand has given its cast of candy characters a modern makeover. “We took a deep look at our characters, both inside and out, and have evolved their looks, personalities and…

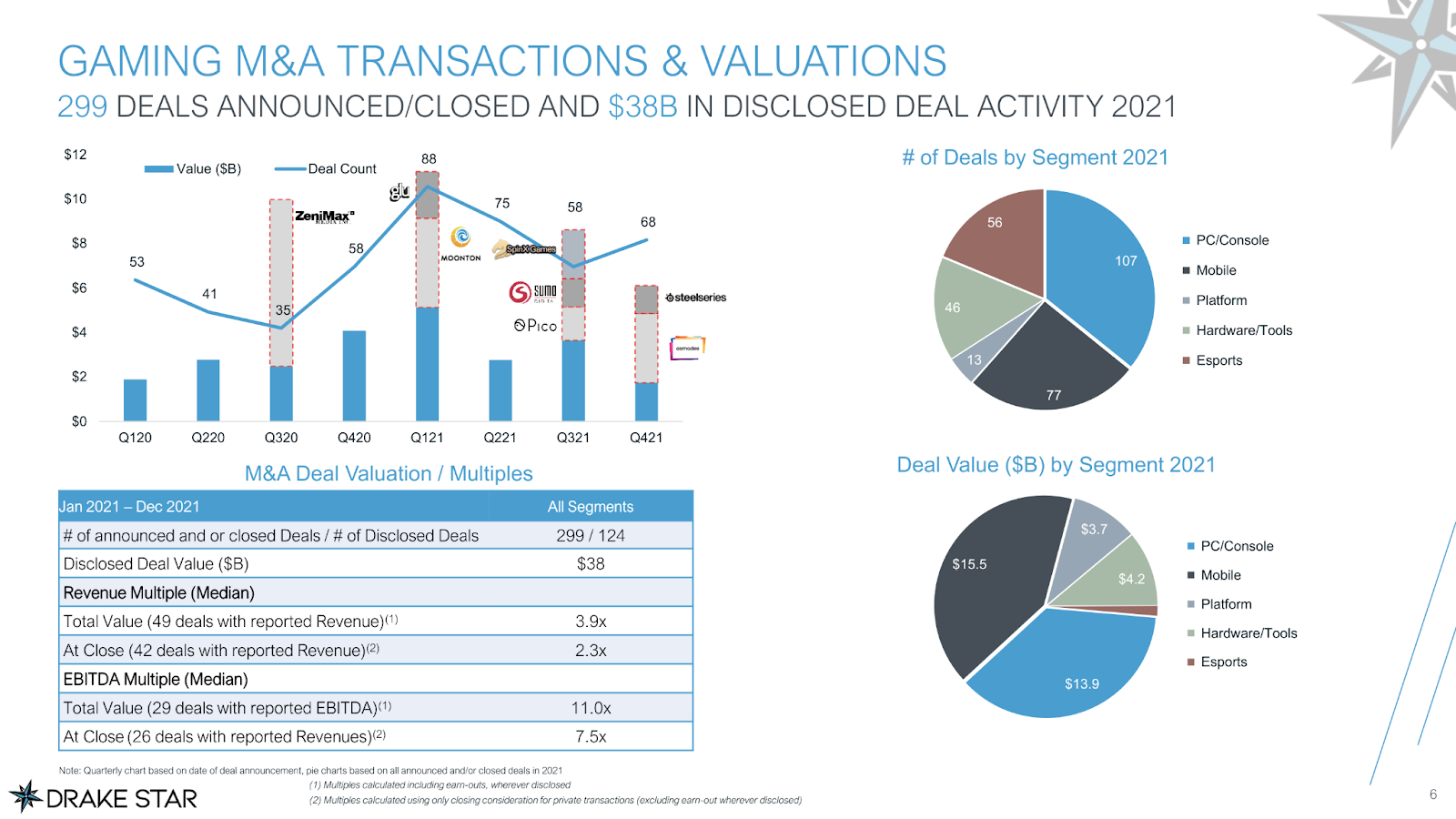

In Graphic Detail: The great gaming consolidation

In Graphic Detail is an ongoing series from Digiday that takes a “show, don’t tell” approach to covering the biggest trends in media and advertising.

Gaming is in the midst of an M&A arms race. The protracted pandemic has made sure of that. Companies from all sides of the market, Microsoft, Take Two, Sony to name a few, are cutting deals to secure content. The volume and scale of those deals point to where gaming is heading — the precipice of major shake-ups across its core commercial and distribution models. Microsoft’s eye bulging $69 billion deal for Activision is a testament to that shift. Costly as the deal is, it’s arguably a small price to pay to secure some of the biggest franchises in gaming: Call of Duty, Warcraft, Candy Crush and Overwatch. Even more so, considering those titles span a community of 400 million active monthly players. In other words, the deal is the boldest sign yet that content is the future of gaming, not consoles.

Here’s what that shift and the M&A wave it kicked up means in graphic detail across five charts.

The gaming industry is going through a period of consolidation unlike anything we’ve ever seen before

Which is to say securing a slice of the industry is becoming table stakes for a lot of businesses. M&A activity generated $38 billion last year, driven by strategic investors such as Take Two, Zynga and EA. On the flip side, private equity firms, venture capital outfits and strategic investors pumped $13 billion into private companies in 681 deals, per investment banking firm Drake Star. It’s a period of consolidation unlike anything the market has ever seen — in line with a flurry of deal activity across the media industry that dates back to 2020. It’s all down to a few underlying factors: Central banks are pouring money into the economy, creating an overheated investment environment: growing pressure to secure content and subsequently strong IP: the big players have more money and more confidence reinforcing their M&A activity. Marketers would do well to watch how this all plays out given these deals will help build the next generation of companies in one of entertainment’s most pervasive categories.

Gaming is the most lucrative entertainment industry by far

Gaming is arguably the largest and most expansive entertainment industry. Not only is it changing the way people interact with each other, more digital activities are taking place inside games. It’s even reshaping the order and power structure in technology, if recent observations are to be believed. Simply put, it’s becoming the dominant entertainment medium for certain demographics. To put that ubiquity into context, the global box office saw takings of around $21.4 billion last year. Gaming, on the other hand, was worth $173 billion in 2021, and $223 billion this year, per GlobalData. And it shows no signs of slowing down anytime soon. On the contrary, the game industry is forecast to grow at 4.4% compound annual growth rate through 2025, according to PricewaterhouseCoopers — though the industry is split between the console market of “core gamers” and the more casual mobile audience.

Gaming’s slow take over of the entertainment world will be funded by advertisers.

Unsurprisingly, advertisers are bringing gaming and esports in-house.

Over the last two years, non-endemic brands have shown increasing interest in the gaming market, with fashion leaders such as Gucci and Ralph Lauren activating inside games like Roblox and Fortnite. For marketers, speed, efficiency and overall, a need for more control has meant some highly publicized attempts to build their own in-house gaming teams that replace — either partial or full agency offerings. Much like ad tech, two lanes exist for doing this: advertisers either assemble a team to manage campaigns in and around games and esports independently, from creator outreach to campaign ideation through to execution and measurement; or they hire an in-house gaming consigliere to mastermind gaming marketing while still relying on agencies to execute those campaigns. Deciding which model to adopt is difficult. There’s much scope for disagreement as the chart below shows.

| Advertiser | Total Net ’20 Media Spend $B | Gaming/esports |

| Procter & Gamble | 7.95 | – Runs sponsorships of professional esports players and online streamers. Also has a team of esports marketers. |

| Unilever | 4.30 | – Sponsors esports events. It hosts monthly gaming master classes in which professional video game players update the company on the latest trends in the sector so they can stay informed. Has said more of its budget will be spent on gaming in future. |

| L’Oréal | 2.73 | – Partners with esports teams and advertises on mobile games. Is exploring product placements in games where the player or the viewer is able to buy what they see through micro-transaction. |

| Amazon | 2.67 | – Owns Twitch and a separate video games division. |

| Nestlé | 2.56 | – Partners with influencers in gaming to develop branded content. Has a team of marketers who broker abs oversee those partnerships and more |

| Volkswagen Group | 2.50 | – Sponsors esports events and teams. |

| Renault-Nissan-Mitsubishi | 2.32 | – All three car brands have a presence in gaming – albeit to varying degrees – from sponsoring esports teams to building an esports gaming rig in a truck. |

| Stellantis | 2.24 | – Is developing software for innovative car features for its drivers including video games for passengers. |

| General Motors | 2.13 | – Building a presence in esports via sponsorship deals with teams and events. |

| Reckitt | 2.10 | – Appointed a global head of gaming in 2020. |

TV is caught between cyclical and structural growth factors

The TV industry, despite how robust its been to disruption, is caught between cyclical and structural growth. Sure, it grew in spurts through the pandemic thanks to events like the European Football Championship soccer tournament and a wider, albeit protracted, recovery of consumer spending. But there’s also been supply chain issues that have dampened ad spending on TV. Predicting what happens next is trickier than ever as a result. What isn’t up for debate, however, is the pandemic has compounded what was already well underway: the time being spent watching TV is being redistributed. Gaming — and the adjacent activities to it — stands to benefit from this as more people choose it as their main source of entertainment. Gaming companies are already beginning to take advantage of this convergence by producing narrative, linear-style content and expanding their offerings into the world of traditional entertainment.

CJ Bangah, a partner at PricewaterhouseCoopers expanded on the point: “Is gaming growing at a fast rate and poised to continue to influence and transform other media categories? Yes. Does that mean television is irrelevant? No.”

The numbers bear this out. Bangah said.

“Globally when we look at the entertainment and media growth rates, video games and esports (5% CAGR between 2021 and 2025) is poised to grow faster than many other categories (including TV advertising: 3%, Traditional TV and home video: -1%, Consumer books: 1.3%), however has a slower growth rate than other categories including OTT video (9.4%), podcast advertising (15.6%) and VR video (16.4%),” she added.

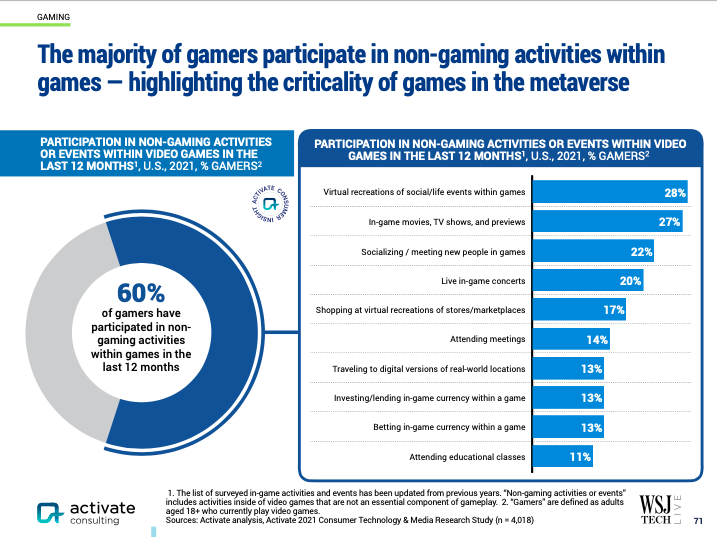

Games aren’t where people go to unwind. Its where they go to hang out

A narrative has been allowed to swirl in media circles that Fortnite, Roblox et al., are the social networks of the future. Sure, engagement and socializing are what makes those games tick but they’re more than just a place to add friends and collect likes and followers. In fact, Fortnite and Roblox are closer to what the theme parks of the future will look like. Not only are they places where virtual versions of people meet up and play games together, they increasingly do everything else there as well, from attending in-game concerts to watching TV shows and film previews. As in-game socialization becomes the norm, it’s clear that leaders are emerging from the gaming space — a trend highlighted by Microsoft’s framing of its acquisition of Activision Blizzard as a bet on the metaverse. As ever, the pandemic has brought this shift into sharp focus, as research from Activate shows.

The post In Graphic Detail: The great gaming consolidation appeared first on Digiday.

‘The business is at a level of scale now’: The Brandtech Group CEO David Jones on building a business for the ‘post-advertising’ world

News that You & Mr Jones is now The Brandtech Group will come as no surprise to anyone who has followed the holding group since its 2015 launch. For starters, founder David Jones has always described his business this way, going so far as to trademark the “brandtech” term. A name change was always on the cards. It’s the timing of it that’s interesting. Not only is the holding group past the hype cycle peak these businesses usually encounter, it’s skipped right over the trough of disillusionment that tends to follow and is straight into growth mode.

Last year, for example, it pocketed $500 million in revenue and could make even more in 2022 if it’s punchy start to the year is anything to go by. Organic revenue growth for the first three quarters of 2021 was 50% more than it was the previous year. And the business seems well placed to keep up the momentum. Aside from the media division it launched last year — complete with a $300 million war chest for investments — it also recruited Will Luttrell, the founder of Integral Ad Science and Amino as it’s chief technology officer.

The growth combined with subsequent investments has left the holding group carefully positioned at a time of immense change for the industry. Whether its Web3 or CTV, in-housing or e-commerce, advances from the group are all in service of a wider model — one that’s diametrically opposed to the legacy holding groups Jones was once part of. Understandably, Jones wants to double down on that advantage. One way to do this would be for The Brandtech Group to become a publicly traded company as Sky reported last summer. Jones, however, is keeping all his options open.

“To be honest, we have a lot of options, this is one of the great things about how well the business is doing,” he told Digiday. “We could remain private, we could make a major game-changing acquisition, we could do another round and raise our Series C or we could IPO. All of those things are potential options for us moving forward.”

Digiday caught up with Jones to hear what this all means for The Brandtech Group in 2022, how that’s influenced by the current concerns of advertisers, why the name swap is happening now, and more.

This interview has been lightly edited and condensed for clarity.

Why make the name change now?

We’re now a big, significant company that’s the largest global partner for many of the biggest companies in the world. We have more than 5,000’; people around the world, there are 18 senior partners, and over half a billion in revenue. The business is at a level of scale now that made the timing right to change the name. More importantly, it’s a move that acknowledges the scale of disruption that’s happened over the last two years but also looks to the future in so far as this post-advertising world we’re heading toward. We’ve already changed four or five names of companies across the group to reflect the brandtech focus, whether its Brandtech Media or Brandtech Commerce, so it’s not hard to imagine the other companies we own undergoing the same thing later down the line. It puts down a marker.

What does brandtech even mean?

When I was drawing up the original business plan for the business, I wasn’t sure what to call what we would offer clients. I settled on this idea of brandtech, given technology is giving brands so many different ways to connect with people way beyond advertising. That hasn’t changed since we launched. Most people didn’t think that would amount to much when we were getting ready to launch the business. Fast forward to today and our thesis has been proven. Pre covid over $30 billion came off the market capitalization of the big five holding companies. We’ve tried to be disruptive to that model and do things differently to those companies; we don’t buy media or ad agencies, for example. We acquire companies in high growth disruptive spaces like in-housing with Oliver.

On the subject of previous acquisitions, what type of areas will you focus future investments on, especially given how rampant M&A is at the moment?

Agree m&a is going to accelerate not slow down. Gravity Road is our metaverse agency and one of the world’s leading companies in this space. Now we’re ramping up these investments in metaverse and are currently looking at one company a day. There are obviously big opportunities when it comes to influencer and people-powered marketing too. Beyond metaverse our core areas of focus are ecommerce, digital media and expanding our capabilities globally. The recent acquisition of [data company] DP6 — Brazil’s number one Google partner — being a key example.

Traditional agency holding groups don’t tend to cut those sorts of deals to the extent you have. Who do you regard as competition?

The big story is the huge shift from the traditional holding companies to the new model companies like ours. Brands today typically have a choice: work with a global holding company, which is everywhere and can deliver globally, but on the whole are not very good at cutting edge tech and tech-enabled marketing, or go around the world picking best in class partners for every discipline in every market where they are good at cutting edge tech and tech-enabled marketing. But the client then has a nightmare job trying to bring that together and coordinate that and make them work together. We deliver cutting edge tech and tech-enabled marketing at global scale and that is typically where and why we are winning our business — 60% of it approximately is coming from brands and clients consolidating in hundreds of digital agencies into us around the world. Last year our second largest client consolidated another 600 digital agencies into us and one of our largest clients started off by doing the same with 3000 digital agencies. We also regularly come up against the Accentures of the world as well as some of the new brandtech companies like S4 and Jellyfish. Not to mention the holding companies who we will often replace when they have tried but failed to deliver state of the art digital marketing solutions. Those businesses are still very good at creating TV commercials and doing traditional media but that is no longer a growth business.

But those businesses have shown signs of improvement of late

Yes, they are growing this year with good growth but it’s the same growth as they declined last year. Trying to shift those services to digital undermines the core businesses of those groups. For example, they would rather sell expensive creative teams than work with open people-powered or influencer models. Furthemore, those businesses have no technology platforms or proprietary tech. And they trade at 1 or 1.5x revenue so can’t afford to buy the new model companies as it’s immediately destructive of value not accretive. Also, the vast majority of the hundred thousand or so people employed at the larger groups are not digitally native. None of the best talent wants to join them any more. They either want to go to the tech platforms or the influencers businesses or companies like ours or start their own. It’s similar for businesses. None of the smartest and best new model companies want to sell to them as they realize the above. We have never failed to acquire a business versus a holding company, for example. The leadership at those businesses doesn’t understand digital and they were born and created not just pre the mobile world but pre the internet.

You mentioned earlier Gravity Road is the group’s metaverse agency. How are marketers responding to this prospect?

I think we are seeing a few things happening: first, people are literally just jumping in without thinking and turning their product into an NFT and putting it on the open sea. This is not a great idea. A bad idea doesn’t become a good idea because it uses the latest technology. It’s still a bad idea. Most of the brands who have done this have not been able to answer the question “why are you doing this?”: second: there are those brands that are doing some smart and interesting things like Stella Artois and [the digital horse racing platform] Zed Run: finally, some brands are using nft’s around purpose like l’oreal or barbie and [French fashion luxury label] Balmain.

Overall, I’m seeing less cynicism from brands, and more experimentation when it comes to how they react to the metaverse and web3 more broadly. No one can say for sure how this transition to either is going to play out. But what we do, through the investments we’ve made, is get a ring-side seat to how it’s all going to play out. [Pokemon Go developer] Niantec is one of the world’s leading meaverse companies and we’ve been an investor since day one, for example.

The post ‘The business is at a level of scale now’: The Brandtech Group CEO David Jones on building a business for the ‘post-advertising’ world appeared first on Digiday.

With Marquee, Jellysmack looks to turn non-digital natives into a new generation of internet stars

Jellysmack, a digital media company and content studio, has proved it knows how to distribute video across the social web. It’s hoping knowledge can mint another generation of hit video creators, using people who got famous for doing something besides posting content.

On Jan. 20, Jellysmack will announce that the UFC heavyweight champion Francis Ngannou has joined Marquee, its recently announced partnerships program where Jellysmack partners with celebrities to co-create social video content. Jellysmack consults and collaborates with partners on the content produced while bearing the costs of producing, editing and distributing the content across a variety of social platforms, ranging from TikTok to YouTube to Snapchat; celeb and studios split the resulting advertising revenue.

The Marquee program is designed to embrace multiple market opportunities at once, using expertise and insights Jellysmack has built up about the vagaries of social video. If successful, Marquee could further extend Jellysmack’s already-large social video footprint, lengthen the list of influential talent it works with directly, and create more opportunities to forge direct relationships with advertisers.

Marquee is also part of an emerging story of publishers and content companies trying to find new ways of connecting to individual creators and personalities, who have become ascendant as social platforms have started maturing as native video content destinations.

“We’re only seeing higher and higher demand for creator economy infrastructure,” said Sean Atkins, who joined Jellysmack as president in September. “We’re still really in the early innings of what’s going to be a multi-hundred billion dollar industry shift.”

Since its launch in 2016, Jellysmack hasn’t built itself into a mainstream media brand, but it has amassed considerable scale across social platforms. Tubular Labs ranks Jellysmack sixth among all media properties by view counts, ahead of much larger companies including WarnerMedia, Comcast and BuzzFeed. It pulled in 6.9 billion views across platforms in November 2021, according to Tubular.

And in recent years it’s been figuring out how to better leverage the scale and expertise that built it. About two years ago it began helping YouTube stars build audiences on Facebook, largely by re-editing and syndicating the creators’ content. That approach brought in stars ranging from PewDiePie and MrBeast to Neil deGrasse Tyson, and it represents hundreds of creators. It offers similar services to media companies and brands as well, selling services designed to help grow footprints across platforms.

Those skills should theoretically come in handy with its first Marquee client as well in Ngannou, who for example, has over 3.3 million followers on Instagram and 1 million followers on Facebook, but less than 165,000 on TikTok and 189,000 on YouTube. Being able to create content that speaks directly to those audiences ought to grow Ngannou’s overall footprint of followers.

“We know what kinds of content will work,” said Olivier Delfosse, Jellysmack’s head of strategic partnerships. “And we know how to make that content in a way that will financially make sense.”

While some of that content will clearly be the work of a production team, Jellysmack is hoping that some of it will feel more personal. “We want it to feel like Francis went out and picked up a camera [himself],” said Aaron Godfred, vp of Marquee.

Being able to create a new constellation of internet stars, ones big enough to attract the attention of main advertisers, feels like a logical evolution for Jellysmack, said Karl House, the chief operating officer of StackCommerce and the former co-founder of Fanbread, which helped celebrities create and distribute content through their Facebook pages. “The brand partnerships are where the big money is,” House said. Jellysmack said it will focus on creator categories including professional athletes and people in the beauty space. It is not clear how many celebrities Marquee might manage.

This is not the first time a media company has tried to help celebrities better leverage the reach their status has provided them on social platforms. Facebook alone has supported a couple of similar cottage industries over the years, ranging from link-sharing businesses that paid celebs to distribute articles to video licensing businesses that proffer user-generated content which can be lightly modified, then published on Facebook for easy ad revenues.

But thanks to years of platforms copying one another, there is now a much wider — and more homogeneous — ecosystem out there for native video content. An engaging series shot on vertical video can now be easily disseminated across Facebook, Instagram, Snapchat, TikTok, YouTube and Pinterest.

But those platforms can change their rules at any time — Facebook effectively wiped out the link-sharing strategy that many publishers relied on by changing its branded content rules — so over time, it will be worth watching how strictly the platforms police their content. For example, Instagram changed its algorithm in early 2021 to stop promoting recycled TikTok content inside Reels, its TikTok knock-off.

But with products including Snapchat’s Spotlight, Instagram’s Reels still in their infant or toddler phases, that might be more of a 2023 issue than a 2022 one.

“For the newer platforms, it’s kind of in their interest not to suppress anything,” House said.

The post With Marquee, Jellysmack looks to turn non-digital natives into a new generation of internet stars appeared first on Digiday.

Media Briefing: Publishers grapple with an existential crisis as they prepare for post-cookie landscape

This week’s Media Briefing looks at why some publishers would prefer to completely reset the online ad market amid the third-party cookie’s demise rather than repeat the problems the cookie introduced.

- Burning for control

- The web’s looming measurement mess

- Marc Benioff and Patrick Soon-Shiong assess their media investments, how the New York Times beat out Amazon and Condé Nast to buy The Athletic, Forbes employees criticize publication for workplace inequity and more

Burning for control

The key hits:

- An email-centric post-cookie identity picture poses a problem for the overwhelming majority of publishers that will lack sufficient scale.

- Non-email-based alternatives like curated marketplaces relying on contextual data present one option for publishers.

- But the ultimate solution may be a complete reset of the online ad marketplace.

The web’s identity crisis is getting “pretty existential,” as one media executive put it.

Some publishers have already come to the conclusion that they will likely never accrue enough email addresses to replace the third-party cookie and satisfy advertisers’ demands for individual-level targeting. That assessment was made even more acute earlier this month when NBCUniversal announced its first-party data platform that the Comcast-owned conglomerate claims to span 150 million individuals.

“Email addresses aren’t going to scale on the open web with publishers like us,” said a second media executive. “For NBC, ABC, anybody with a CTV or streaming [property] or anywhere where you have to authenticate every time you use it, those are the people who will win in identity.”

The first media executive recalled a recent conversation with an executive at a large telecom company that had set a goal of accruing 40 to 50 million members of its existing customer base to opt into that company’s first-party data platform. “I think they got to 9 million,” relayed the media executive. Perceiving that this telecom would have had an advantage to load up on first-party data but only cracked 20% to 25% of its goal, “maybe the rest of us should not be chasing the scale game.”

“As marketers want to get more specific and understand and identify their audiences more, we’re going to struggle to figure out how to do that based on the scale of, essentially, the internet,” said a third media executive.

“On the data front, none of us have the scale of an NBC or a large TV player,” said a fourth media executive.

Where does that leave the broad swath of publishers then?

“Publishers should really consider burning the whole thing down,” said a fifth media executive. This person was joking. Sort of. While they and other media executives are not intending to torch the online advertising marketplace, they are hoping for something akin to the controlled burns that Native American tribes had conducted to avoid widespread wildfires and spur plant growth.

One way that could manifest is through publishers themselves opting out of email-based cookie alternatives. Some, like Insider, BuzzFeed and Group Nine, already are by refraining from building their respective first-party data platforms around email addresses. Others are looking to move more of their inventory from open programmatic marketplaces to curated marketplaces.

Operated by ad tech firms like YieldMo and GumGum and even by publishers like Vox Media, which has Concert, curated marketplaces only offer inventory from selected publishers, sometimes grouped into category-specific segments, and base their targeting on contextual data, like the keywords on the page carrying an ad.

“I see [a curated marketplace] as somebody who’s bringing attention to my inventory in a marketplace that I have a lot of control over. Because I do set floor pricing, I do set the rules of engagement for it,” said a sixth media executive.

Some other media executives, however, were more skeptical of curated marketplaces. These media executives were generally wary of exposing themselves to outside companies altogether. That includes the companies operating curated marketplaces but also the companies proffering alternative identifiers.

“This is about control and access to scale. To do it by allowing people to scrape your pages or put code on pages that you don’t feel as secure about or you don’t know what happens with the data, that’s a challenge for publishers,” said the second media executive.

“The risk is probably less technical and more strategic in the sense of, if your data is in a pool of data, does that diminish the value that you could have if it was truly only available in a standalone way? And if so, what are those trade-offs?” said the first media executive.

The overarching risk for publishers is a post-cookie landscape that features the ills that the third-party cookie introduced for publishers. The third party was initially adopted as a means of enabling publishers to band their inventory and audiences together to satisfy advertisers’ growing demand for individual-level targeting at scale, which they had gotten a taste for from Google and Facebook. But over time it enabled ad tech intermediaries to intercede in publishers’ dealings with advertisers and resulted in publishers’ inventory being devalued. And now it may be happening all over again.

“There’s just so much fucking ad tech middleman stuff, excuse my French. So much,” said the fifth media executive. “It’s like, every single time there’s a change, we just come up with a new way to give some guy in the middle a bunch of money.”

So, again, the question of where does this all leave publishers? Inching closer to the flames, it seems.

“There’s going to be a whole rebirth of all this stuff, I think,” said the third media executive. “Hopefully.” — Tim Peterson

What we’ve heard

“Diversifying into food [as a content category] is really big. It’s got super high RPMs relative to everything else. It also has a higher success rate for internal recirculation than other verticals do. We find it as a very good second article for most people on the site.”

— News publishing executive

The web’s looming measurement mess

Publishers are not isolated from the measurement overhaul sweeping the media industry. As TV networks and streaming services work to wean themselves off Nielsen, publishers are having to confront how the third-party cookie’s demise will impact the measurement of ads on their sites.

“We need to rethink how we’re talking about measurement, how we’re doing it,” said one publishing executive.

Online publishers have relied on the third-party cookie as a means of measuring how the ads running on their sites perform for advertisers, from gauging brand effectiveness to attributing product sales. But in roughly a year and a half, that method will be effectively taken off the table when Google disables third-party cookies in its dominant Chrome web browser.

So what are publishers to do? The answer — like many things cookie-related — is unclear. Cookieless measurement options for web publishers appear hard to come by at the moment.

“I’m worried about the dearth of measurement solutions at scale for the open web, which has the potential to put us and other digital publishers behind the eight ball,” said a second publishing executive. — Tim Peterson

Numbers to know

$68.7 billion: The price Microsoft paid to acquire videogame company Activision Blizzard, which, if it goes through, would be the tech company’s biggest-ever acquisition to date.

$16 million: The amount The Arena Group (a digital publishing company formerly called Maven) paid to buy AMG/Parade, which publishes Parade Magazine.

7: The number of Chicago-based G/O Media employees who were told to relocate to Los Angeles, without a cost-of-living adjustment, or lose their jobs. All seven employees decided to take their union-contract-protected severances rather than make the move.

$60,000: The new salary floor for New York Magazine’s union workers after the union reached a deal with the company for its first contract, after more than two years of negotiations. More than half of the staff will receive a pay increase, with some employees earning up to $20,000 more than they previously were.

$599: The price of an annual subscription to Axios’ new Pro Deal newsletter business.

What we’ve covered

Where publishers see revenue growth in 2022:

- For all the progress publishers have made in diversifying their businesses, many of them head into 2022 more optimistic about their advertising businesses than the revenue streams that complement them, according to new Digiday+ research.

- Yet there are nuances to how that optimism is distributed. Among publishers that consider subscriptions to be a primary source of revenue, for example, a greater share are optimistic about their subscription revenues growing than the share that’s optimistic about their ad revenue.

Read more about trends in anticipated revenue growth here.

Why media unions are demanding to participate in management’s return-to-office planning:

- Nearly two years since the pandemic began, media employees are still dissatisfied with their companies’ plans to bring them back to the office. For many media unions, the latest battleground is not the fight for wage increases or promotions: It’s the return to in-person work.

- Media unions demand management come to the bargaining table over RTO plans and are fighting back against office return mandates and dates.

Read more about the conversations around return-to-work here.

WTF is Web3?:

- “Web3” is the latest label to describe this next era of the internet, but it’s unclear whether publishing execs are aware of just how much it has the potential to impact business in the coming years.

- Web 3.0, or stylized as Web3, is the label being applied to a decentralized version of the internet that would be jointly owned by the users and the builders. Essentially, this is the antithesis to how centralized platforms like Apple, Google and Facebook operate, by monetizing data extracted from users on a daily basis.

Read more about Web3 here.

How Leaf Group transitioned to being a commerce-dominant media company:

- Over the past eight years, Leaf Group (formerly known as Demand Media until 2016) has transformed itself from a SEO-focused content farm to a commerce-driven media company that sold for $323 million to Graham Holdings last June.

- Much of that transition was done at the hands of CEO Sean Moriarty, who wanted to build a portfolio of expert-led content that readers turn to when making purchases.

Listen to the latest episode of the Digiday Podcast here.

Recurrent Ventures — the next big private equity-fueled media conglomerate?:

- Recurrent’s modus operandi — acquire mostly struggling, legacy enthusiast media brands, centralize non-edit resources while preserving editorial departments — seems to be working so far.

- The company tripled its revenue in 2021, and CEO Lance Johnson expects a profit margin of more than 20% for the year, though he declined to share specific figures.

Read more about Recurrent Ventures’ 2022 growth strategy here.

What we’re reading

Vanity purchase or strategic play, Marc Benioff is in the process of transforming of Time:

Nearly four years after buying the legacy magazine from Meredith, Axios reports that Time is projecting 30% revenue growth this year, amounting to over $200 million. CEO and editor-in-chief Edward Felsenthal said that approximately one-quarter of that revenue is coming from its studios business, which is just two years old.

$1 billion in, Los Angeles Times owner Patrick Soon-Shiong talks about his investment in the newspaper:

Four years after pharma executive, Dr. Patrick Soon-Shiong purchased his “local newspaper,” the Los Angeles Times, for $500 million, he said he wants this business to become his family’s legacy, the Press Gazette reported. To prove it, he said he has invested hundreds of millions of dollars into modernizing parent company California Times group (which includes the L.A. Times and the San Diego Union-Tribune), amounting to close to $1 billion of investment.

Sports reporters are relying on Twitter to reach the masses:

NBA sports reporters Shams Charania and Adrian Wojnarowski have assembled massive followings on Twitter, and those followers are closely watching their feeds for the latest news of trades, injuries or free agent signings in the industry, according to CNBC. Because of this, Charania, Wojnarowski and other journalists in a similar position are being courted by media companies who want to benefit from their fan bases.

Inside The New York Times’ acquisition of The Athletic:

Before the sale of The Athletic was finalized, The New York Times increased its offer by 10% to beat out Amazon, Condé Nast, DraftKings and private-equity firm TPG Capital, according to CNBC. Despite the sports publisher never being profitable and burning through $100 million between 2019 and 2020, the bid for The Athletic reached $550 million.

Despite reporting on wealth, Forbes’ employees claim they’re underpaid and overworked:

Forbes has built its reputation as a media company by celebrating business success and wealth. However, Insider reports that employees of the publication say they’re facing workplace inequity, working long hours and are being compensated at low rates. With the publisher’s upcoming IPO, some are doubting whether or not going public will benefit staffers.

The post Media Briefing: Publishers grapple with an existential crisis as they prepare for post-cookie landscape appeared first on Digiday.

Axios schedules its largest in-person event for April (for now)

Like many media companies, Axios is in the process of scheduling its 2022 events calendar and has set its first in-person event of the year to take place at the beginning of April.

The event is expected to reach a couple of milestones as it is projected to be the largest event the company has hosted in its five-year history and only the second in-person event since the pandemic began in March 2020 (the first was its 5G Forum in November last year).

The What’s Next Summit will take place on April 5 and 6 in Washington, D.C., and was born out of Axios’s What’s Next newsletter product, which was first published in summer 2021. The newsletter covers how the pandemic has changed in how people work, play and get around, and the conference is aimed at getting executives from a number of industries to talk about the challenges and changes they’ve experienced in these areas, said Sara Kehaulani Goo, editor-in-chief of Axios.

The summit, which is expected to become an annual event, will have virtual components, with the mainstage panels being broadcast via a live stream, but the in-person elements of the conference will be a core part of the programming. The event will be free to attend and watch. If omicron persists or another variant threatens the safety of the event, Axios will move it to a later date so the in-person elements, like small working groups and roundtable discussions, can still happen in person, said Kristin Burkhalter, the company’s svp of events and creative strategy.

About 220 people are expected to attend the summit in person, all of whom will be invited from a curated list of leaders that is composed by Goo’s editorial team and do not have to pay to attend, according to Burkhalter. An even smaller selection of those invitees — about 120 people — will be able to participate in the in-person working groups, to limit the number of interactions between guests, but also to focus on solving the specific issues each participant brings to the table more efficiently. All attendees will be required to show proof of vaccination, as the company is adhering to Washington, D.C.’s vaccine guidance, according to a company spokesperson.

Because the in-person element is so crucial to the success of the summit, in Burkhalter’s and Goo’s eyes, flexibility around the date will be necessary to orchestrate the event safely for attendees. Getting sponsors on board with any changes to that schedule will be just as important, however, as they are the sole sources of revenue for this event.

Right now, there are four sponsors signed on for the event, including Meta and Density, all of which are doing an in-person activation. Burkhalter said it was an “all or nothing” deal with the event advertisers, meaning none could opt for a virtual-only sponsorship. Keeping the sponsor list limited kept the focus on the editorial programming, she said, and the spots available were reserved to the brands willing to pay for the in-person activations. Axios did not disclose how much each sponsor paid to be a part of the event.

Key to getting sponsors to agree to the “all or nothing” arrangements was Axios vocalizing the contingency plans for the event and defining that clearly in the contracts, Burkhalter added.

Flexibility is a requirement in conversations around event sponsorships, according to a former media agency executive who asked to remain anonymous due to a recent personnel change. “No one is going to commit a lot of money without flexibility and if [a publisher] isn’t going to offer it, you have to offer a great package” with additional digital components.

Last year, Axios hosted more than 100 virtual events and one in-person event, which increased the revenue of its events business by 41% from 2020 to 2021, according to the company. All Axios events are free to attendees and rely solely on sponsorship revenue. The company’s virtual events tend to include only one sponsor per event. The expectation is that revenue from this side of the business will continue to increase this year as well. The publisher’s events team consists of 13 employees.

In general, brands have been eager to return to in-person events, even in the recent context of the omicron variant.

There were fewer events taking place in-person during the first quarter of the year than originally expected hosted by publishers or in general, according to Grant Ogburn, svp of experiential at experiential agency Hawkeye, but the second quarter through the end of the year is already booked up for the agency. Not only that, but the number of RFPs for in-person events has increased substantially between 2021 and 2022 with budgets for events remaining the same or increasing over last year, he added.

New York-based experiential agency, Makeout NYC — which works with media companies like Time to produce events — is focusing primarily on in-person projects because the budgets, and therefore revenue, is notably higher than what virtual events offered.

“We’re really only trying to take projects that are first and foremost in-person events,” said Eric Fleming, co-founder and executive producer of Makeout. “But we recognize that we’re still going to need [to do] hybrid and virtual only” to provide the cost-effective scale that so many brands have grown accustomed to over the past two years.

The post Axios schedules its largest in-person event for April (for now) appeared first on Digiday.